Charles Marohn is the founder and president of Strong Towns, an organization that leads and supports the sort of bottom-up community-strengthening action we advocate here at Epsilon Theory. He is a professional engineer and a land use planner, with a bachelor’s degree in civil engineering and a Master of Urban and Regional Planning, both from the University of Minnesota. Marohn is the author of Strong Towns: A Bottom-Up Revolution to Rebuild American Prosperity (Wiley, 2019) and Confessions of a Recovering Engineer: Transportation for a Strong Town (Wiley 2021).

You can contact Chuck at [email protected] and on Twitter at @clmarohn.

As with all of our guest contributors, Chuck’s post may not represent the views of Epsilon Theory or Second Foundation Partners, and should not be construed as advice to purchase or sell any security.

There are two different conversations taking place about housing. One happens in the world of housing advocacy. In this conversation, housing prices are seen as too high, and so the conversation tends to focus on how to bring housing prices down. The other conversation takes place in the world of finance. In that space, high housing prices are a feature, not a flaw. The financial conversation focuses on finding more ways for people to access debt.

It is my observation that the housing conversation tends to demonstrate a rather unsophisticated understanding of the financial conversation. That is the case with the simplistic supply/demand assertion that we can build our way to falling home prices. It also shows up in the widespread assertion that developer greed is the primary source of rising prices. While I share a lot of the same underlying motivations, I have personally struggled to engage with the housing conversation because I find it internally incoherent.

That is not the case with the financial conversation. The financial world, a world of predator and prey, is very coherent when it comes to housing. And very sophisticated. Those in the financial world see themselves as the predators. Those seeking housing are the prey. The sophistication comes with how the predators construct and market their financial products to the prey, as well as to the various mediators, go-betweens, and overseers that foster these transactions.

For example, in the 1990s, the Clinton administration created a collaboration called the National Partners in Homeownership (NPH). It was an unprecedented collaboration of regulators and the regulated, federal departments like Treasury and the FDIC and private sector organizations like the Mortgage Bankers Association and America’s Community Bankers. The goal of this initiative was to increase home ownership levels by making homes more affordable for more people.

To that end, they merely expanded the playbook first developed in the Great Depression and then redeployed during the first decades of the postwar Suburban Experiment. For example, NPH called for a reduction of down payments. Fannie Mae — at that time a privately-owned Government Sponsored Entity (a private business with government backing) — responded by reducing down payment requirements from 10% to 3%. In 2001, Fannie Mae entirely eliminated the need for a down payment on mortgages they purchased.

Obviously, lower down payments means less skin in the game for home purchasers, which means greater risk for lenders. The NPH called on the insurance market to address this risk by expanding the use of private mortgage insurance. Insurers such as American International Group (AIG) stepped up their issuance of these policies. (Spoiler: That didn’t end well for AIG or for the federal government.)

Another NPH innovation was the credit score. Up to this point, qualifying for a mortgage meant meeting with a banker for a very intimate and very intense underwriting process. With one human sitting in judgment of another human’s ability to assume a mortgage, all of the human failings — all of the -isms — crept into the process. An algorithm that calculated a credit score for each borrower was considered a much cleaner way to evaluate worthiness.

Conveniently, it was also a great way to issue more debt, especially to poorer people. Frank Raines, who was the chairman of Fannie Mae at the time, claimed that “lower income families have credit histories that are just as strong as wealthier families.” LOL. Raines put Fannie Mae’s (government backed) money where his mouth was by increasing the amount of ultra-low down payment mortgages Fannie Mae purchased by 40 times in the 1990s.

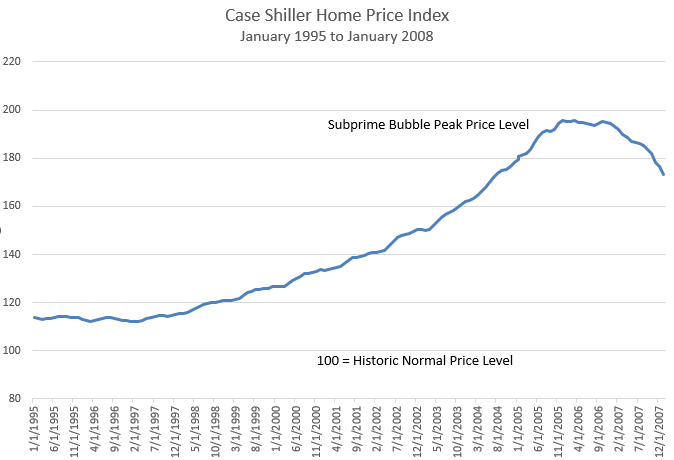

With others joining in, the housing market soared, both in terms of the number of people who purchased homes (goal achieved) and the price of that housing (goal achieved). Here’s the Case Shiller home price index from 1995 through the start of 2008.

This orgy of debt and price appreciation didn’t end well for Fannie Mae. Or, perhaps it did. In September 2008, as one part of the larger subprime housing crisis, Fannie Mae was rescued / nationalized, placed under the control of the federal government. It has remained nationalized for more than 15 years now.

Last month, Fannie Mae announced the launch of a “Single-Family Social Bond Framework,” a set of criteria used to create a financial product they call a Social MBS. This is marketing to investors, letting them know that they can feel good about putting their money where their heart is. By investing in Fannie Mae’s Social MBS, investors are helping allocate more credit in support of affordable housing so that “more people have better access to credit.” Fannie Mae’s marketing suggests they are working on the challenges of the housing market, especially those challenges “that disproportionately burden lower- and moderate-income borrowers and renters.”

This is the kind of thing you’d see in a Super Bowl commercial, complete with a compelling profile of the family being assisted by Fannie Mae’s lending program. It is also the kind of marketing that soothes the concerns of many housing advocates, just enough to keep the focus elsewhere (like those greedy developers). Show me the numbers, Fannie Mae, and they responded with a Social Index Score that does just that. It’s great marketing.

Once again, in the name of having more people take on more debt to pay more money for more homes, Fannie Mae is lowering down payments and extending loans to people with little to no equity and marginal credit scores.

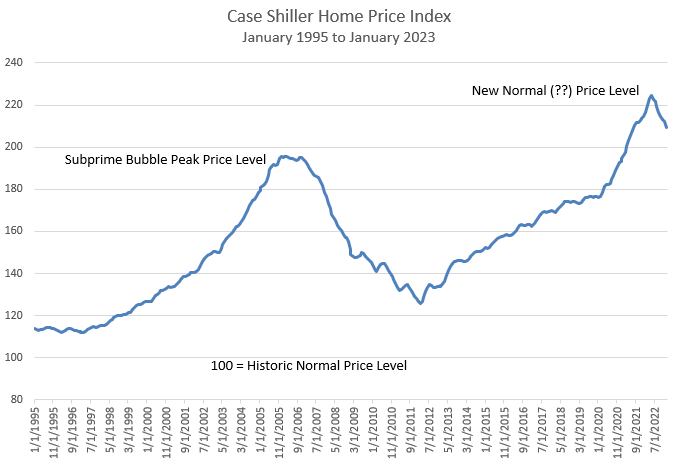

If this seems insane, it is, but understand that 2008 wasn’t the first time we tried this. It was just the biggest bubble this set of strategies had created. That is, the biggest bubble up to that point. Here’s the Case Shiller Index as of the end of 2022.

Want a real commercial, not the kind you’ll see during the Super Bowl but the kind experienced in cities all across North America?

In Detroit, there is a house occupied by a family paying rent to a landlord. That landlord acquired the house through the tax foreclosure process. The landlord may have paid $15,000 for it at a tax auction; the family now pays $700 a month to live there. It is likely that the same family paying rent now was living there when the prior landlord — whose business plan included not paying their taxes — defaulted and lost the home in tax foreclosure, a process that takes 5 years in Michigan (in this instance, not paying your taxes for five years is simply a wise business strategy).

Take the $15,000 purchase price and divide by $700 per month in rent. That’s a tad more than 21 months, less than two years. The family living in that house could have owned it outright in less than two years had they been the ones to purchase it. So, why didn’t they?

The answer is simple: there is no financial product to facilitate that transaction. Fannie Mae, despite the marketing of a Social Good MBS, is not going to purchase that mortgage. The margins are just too small. They won’t purchase it and so nobody originates it, that’s how vertically oriented local banks are. There are hundreds of thousands, perhaps millions, of these transactions that could happen — all of them profitable and socially beneficial — but Fannie Mae has no real financial incentive to bundle them up, securitize them, and create a secondary market for their purchase. So, they don’t happen.

And not only are the margins too small, a proliferation of this product — an entry level housing product at a much lower price point — undermines the entire foundation of housing finance and, by extension, the entire foundation of our banking system (because securitized mortgages make up such a large percentage of bank reserves). It undermines everything because such a broadly affordable product will slow, perhaps even reverse, housing price appreciation. That is also bad for Fannie Mae.

Fannie Mae, and all the other purveyors of centralized capital, are not interested in pursuing strategies that make housing broadly affordable. In fact, they will oppose any policy that actually makes prices go down. They are happy to provide more loans to more people, to increase the amount of debt we consume as a society, because that makes housing prices go up, which is what centralized capital requires.

And they are happy to listen to the housing advocacy conversation, if only to discern just how to market their financial products in the most socially affirming way possible.

This whole thing won’t change until that Detroit family can easily finance the $15,000 foreclosed home they are paying rent on, a transaction that requires less capital than most auto loans. This is not a liquidity problem. It won’t be solved by lowering interest rates or printing more money. It can’t be fixed by originating more mortgages to securitize, by lowering down payments, or by extending terms to riskier borrowers.

It will only be fixed by changing the narratives we have about capital allocation. It will only change when we reject things like Bitcoin!(™) and insist on a real bottom-up exchange of value between individuals. We have the power right now to make that change because we have the power to think clearly, to opt out of the central narratives, to work together with neighbors in each of our communities.

As Ben is fond of saying, “Clear Eyes, Full Hearts, Can’t Lose” is not an answer. It’s a process, one open to all of us.

")

Thanks Charles Marohn for your clear explanation.

Hi Charles, dumb question time:

I have $15k I want to invest. I don’t really trust the stock market or most other big impersonal stuff that mainstream finance gurus tell me to buy.

What mechanisms, if any, already exist for me as an individual to go around all this Sallie Mae ESG nonsense and just loan this family $15k, at terms we can agree on, to finally buy their own damn house?

Surely some mechanisms already exist and are just underappreciated? Keeping in mind there are millions of Americans just like me who are tired of impersonal shell games, have some fun money to invest now, and do understand the risks including possible full loss of principal.

I wish that existed. I mean, if you know the family, you can buy the house at auction yourself and then sell it to them on a contract for deed. But, to do this at scale, somewhat anonymously… don’t know.

I want to take a sec to kind of invert this scenario in a way.

Now that I’m retired I’ve kind of immersed myself in volunteering for Habitat for Humanity; day-to-day nail-bending, dirty fingernails, sore-muscles-from-climbing-ladders stuff. I believe very much in two things; the relationships that come from working for and with others, and Habitat’s foundation of building equity.

That said, in the course of some of those relationships I have come to believe that the model of one family / one single family house leaves a ton of people unserved. The concept of something more like micro-equity and Housing First has come up in discussions, and the idea of the 15k loan or even building equity in a motel room has a lot of appeal in my mind.

Incidentally the local Habitat affiliate I work with uses USDA as a financing source. May be of interest.

I measure once and cut twice. I don’t know much about the money side.

perhaps a dumb question: how is buying a house at a foreclosure auction different from getting a mortgage to buy a house normally? why can’t the family renting treat the rented home as a newly-bought property and use the usual mortgages?

My understanding is the foreclosure auction process involves cash only. This dynamic shuts out the majority of renters who might purchase that asset. Adding a mortgage to a real estate purchase is usually part of the standard closing process, where securing the loan and appraising the property stretch out the closing timeline. Getting a loan secured by the housing asset after purchase means cash closed the deal. Investing in that order (buy then arrange financing) involves some duplicate fees but is often attractive to the seller who has fewer contingencies that could derail the closing. The cash buyer has been making it difficult for first time home buyers who will be using a mortgage to compete.

Thank you for sharing, I was unaware of the new product, but I agree with your conclusions:

I’ll also add that the NIMBY (Not In My Back Yard) element and it’s influence on local politics and zoning laws are arguably one of the other largest issues towards actual affordability. In most jurisdictions density requires “rezoning” and public hearings and decisions by local elected officials, where sprawling single family home subdivisions are typically “by-right” decisions (as long as the developer meets zoning requirements). Thus density very quickly becomes a political football for the local elected officials that want to be re-elected and something to be avoided.

In my neck of the woods, NIMBYs have been replaced by BaNANAs – Build Nothing Anywhere Near Anybody.