Access the Powerpoint slides of this month’s ET Pro monitors here. Access the PDF version of the ET Pro monitor slides here. Access the underlying Excel data here.…

If you’re buying or selling the market because the China deal is on or because the China deal is off, you’re no different from everyone who had a ticket at the Derby. Good luck with that.

Also, what do Warren Buffett and Dune’s Leto Atreides have in common? They both get transformed into near-immortal creatures. I suppose a Cartoon cut-out is more attractive than a sandworm.

Wage stagnation in 2016 was actually much worse than you were told. Did this make a difference in the Midwestern states that swung the election, in that actual labor conditions were worse than everyone thought they were? I think yes.

Wage growth in 2018 was actually much better than you were told. Did this make a difference in the current Fed/Wall Street/White House narrative that inflation is dead and the easy money punchbowl can be maintained without consequence? I think yes.

It’s the Weekend Zeitgeist, in which we consider a going-forward rule for infrastructure editorials, a different kind of Valley Girl, an emerging Get Out of Dodge narrative, and SEO as a service.

It’s the Friday Zeitgeist, in which people who will never buy a company learn how to do it, Powell delivers a belly-rub and takes away a child’s cookie jar simultaneously, Swiss francs climb the Zeitgeist ladder, a local bank makes it up on volume, and we all declare together that an OK faux-hamburger is more than just a faux-hamburger.

Content placement by asset managers is like the elaborate red pouch of the male frigate bird. It is SO wasteful and extravagant that – in an economically perverse way – it demonstrates your evolutionary fitness.

Ditto for why the sell-side still cares about II ratings and “who’s the ax?” and all that stuff that hasn’t mattered for 20 years.

It’s plumage.

At some point, all Fed Chairs learn that their primary function is just to wave their hands. Jay Powell has learned this sooner than most.

ET contributor Pete Cecchini goes way off the Wall Street reservation with this: the bullish narrative for U.S. equity risk makes sense only if one accepts a narrative that the Fed will proactively move to prevent a U.S. slowdown before it happens.

Don’t believe it.

Berkshire Hathaway’s financing for Occidental is in the Zeitgeist today.

What is shadow banking? THIS.

Not that there’s anything wrong with it. Hey, this is Uncle Warren’s true face, and I’m a fan of authenticity in all its forms and ways. But if you think poorly of a guy like, say, Ken Griffin because you think Citadel was “bailed out by the US taxpayer”, and you don’t think EXACTLY the same about Warren Buffett and Berkshire Hathaway … then you’ve been played.

It’s the Tuesday Zeitgeist, in which we explore how you could go with this (or you could go with that), the power of AS, my respect for you, IPOs aplenty and the trade/rotation of choice.

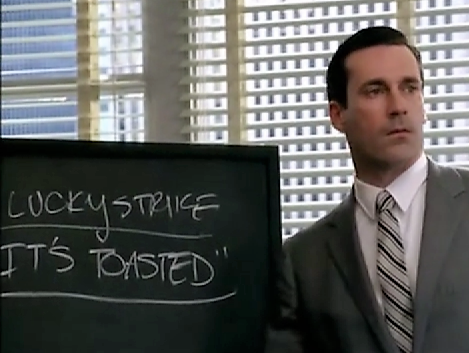

When Donald Trump tells you that there’s no inflation, that up is down and black is white, that monetary policy … It’s toasted! … you’ve gotta believe him, right? Right?

Actually, for investment purposes, you do. When everyone knows that everyone knows that inflation is dead, that IS the Common Knowledge. And the common knowledge must be respected.