Dave Nadig has forgotten more about ETFs and how they work than I will ever know. He co-founded Cerulli Associates in the early 1990s, went on to be Managing Director at Wells Fargo Nikko before selling the firm to Barclays to form BGI, before THAT got bought to become Blackrock/iShares as it exists today. In the early 2000s Dave joined what would become ETF.com, where he helped build their ETF Data and Analytics business which was sold to FactSet in 2017 or so. Most recently Dave was part of the team that formed and sold VettaFi to the TMX group from 2020 to 2023. Dave is currently an "independent financial futurist" and will tell you what that means as soon as he figures it out!

You can contact Dave at [email protected] and on Twitter at @DaveNadig. As with all of our guest contributors, Dave’s post may not represent the views of Epsilon Theory or Second Foundation Partners, and should not be construed as advice to purchase or sell any security.

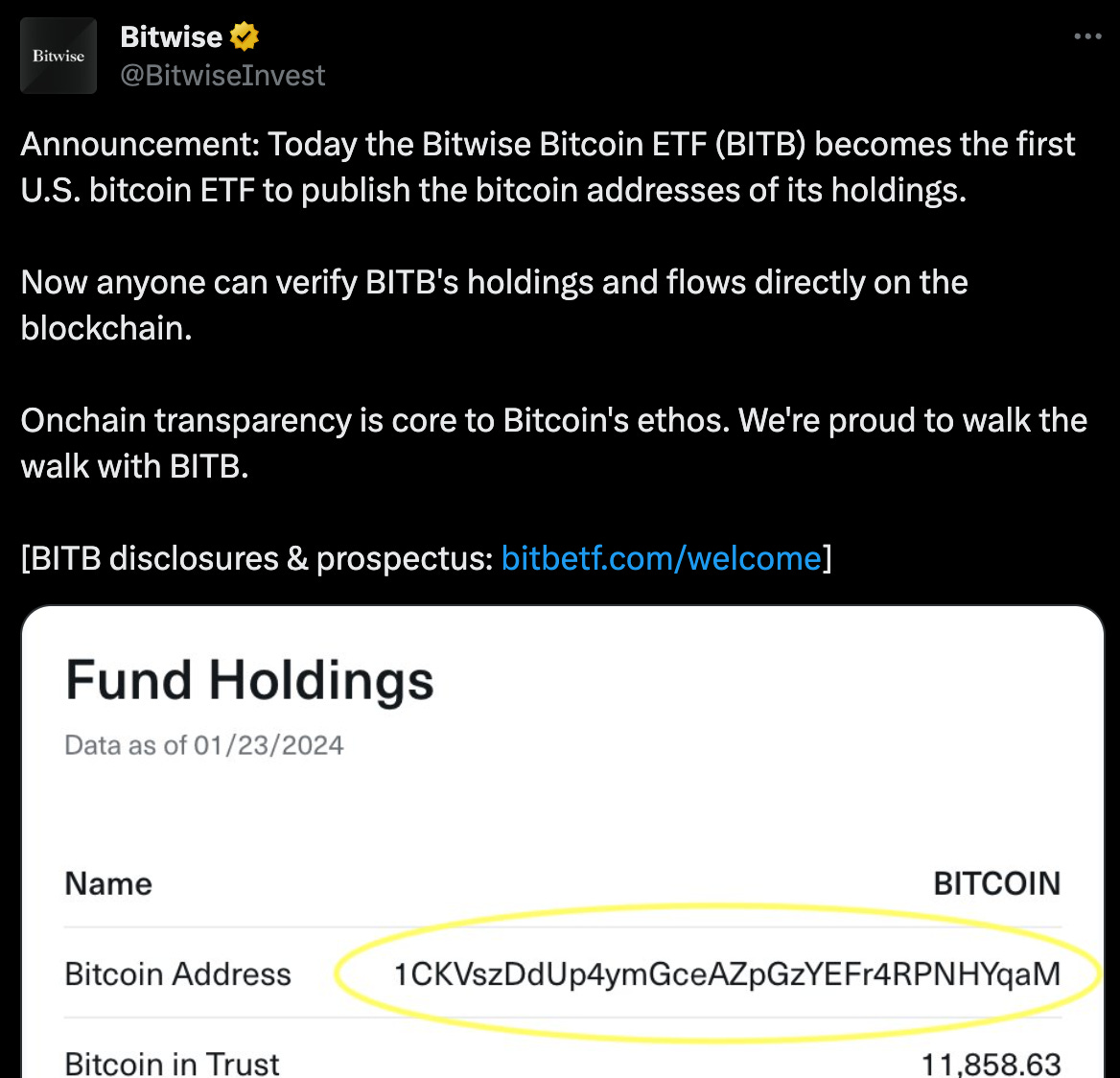

Matt Hougan of Bitwise and I first worked together in 1997 or so as part of “OpenFund - the World’s First Transparent Mutual Fund!” While we got shellacked, it’s not a surprise to see Matt and the team at Bitwise carrying the twin torches of “institutional quality” and “radical transparency,” which they refueled last week with this fun little move:

My first thought on seeing the wallet address out there was “OK, that’s clever… after all, it’s a one-way door, it doesn’t make anything less secure, and instantly solves the tired “there's no gold in the vault” insanity that’s plagued GLD.” (Which mindboggling is still going on to this day.)

What I hadn’t expected was that within hours, someone had just sent random bitcoin to this address:

Hong Kim is the CTO at bitwise, and I thought he did a good job of explaining things in a tweet, but since a bunch of folks asked, here’s my interpretation of the details and some of the fun implications.

The Big Questions

- How the heck do you account for “donations”? Because I’m me, my immediate question was how this gets handled on the books of the fund. I’m pretty conversant in basic investment accounting principles, but not an actual CPA or lawyer or anything, but I stay up on GAAP changes (general accounting), the Uniform Principal and Interest Act (some Trust accounting) and the various interpretations for ETFs over the years, and I’m really pretty darn sure that the few hundred bucks showing up on the BITB books will have to be recorded as miscellaneous investment income on the funds Statement of Operations. Essentially adding a line we never see on, say, GLD’s annual:

- Who Gets It? Because the Bitcoin ETFs are all essentially structured like GLD - Grantor Trusts that cleave to the “Widely Held Fixed Income Trust” IRS interpretations (could be wrong) - there’s not traditionally a dividend mechanism for distributing this “income” out to investors regularly, like there is in a more normal ‘40 Act fund. That’s only a problem to the extent that the amount of donations exceeds trust expenses, which, in a non-waiver period, seems exceptionally unlikely. Theoretically, someone could donate an enormous amount of BTC to the fund, and thus put the trust in the odd position of having to report income that they have not distributed (triggering a tax event for shareholders), or of having to actually distribute the income, which also seems insane and to my knowledge has never happened in Grantor-Trust structured ETPs. So: income, which will be offset by expenses.

- Is this a threat? One wild idea I heard was that some bad actor could try and “poison” BITB or another ETF by routing a bunch of BTC through a sanctioned address and then sending it to the fund. The theory was that this would put the fund in some sort of illegal state, and tie it up with clawbacks and legal shenanigans. It’s an interesting idea (although I have no idea how one would do it or why one would want to), but if you dig into the Coinbase Custody agreements (or just their 2023 consent agreement with NY State) that’s just not how it works. As a big-boy institutional custodian, Coinbase siphons off anything from sanctioned addresses into a penalty box. As far as the Trust is concerned, no “bad” bitcoin ever goes anywhere near the fund — that’s for the Custodian to sort out with the Feds.

- Is it in NAV? This one I am 100% sure of. Once Coinbase has allowed the donated BTC through to the custodial account without being flagged for sanctions, that BTC is absolutely an asset of the trust and will be in the very next NAV calculation. In this case, $400 isn’t going move the penny on NAV. But if someone just “gave” the trust $400 million or something? Sure. It’s in the NAV.

- What about the NFTs!? Believe it or not, this is a thing. If you haven’t been paying attention to the NFT market, the new hotness for the last year has been “ordinals.” Every Satoshi (a 100 millionth of a Bitcoin) has a serial number from when it was minted. These days, you can embed some content in the process of minting a Satoshi, and that means you can make a crude, fully embedded NFT (not just a pointer to a JPG) - as long as the digital thing your inscribing on the Satoshi is less than 4MB. Turns out, a bunch of folks sent BITB some of them too.

")

Long time listener first time caller. Happy to entertain any questions!

UK and EU brokers are not permitted to retail ETF shares. The reason cited is lack of KID provision. Looks like market protectionism to me, as the degree of transparency and research is an individual investor’s preference.

Not sure what you mean? UCITS ETFs are a big deal in the UK/EU for retail? I believe, for example, that every iShares UCITS ETF in the UK has a KIID document and is available at most brokers?

And HL, the biggest broker trades thousands of different ETFs I believe?

I’m sure you’re making a different point though? Are you saying it’s hard for them to sell you US listed ETFs? Or that you can’t buy local Jersey/German/Swiss BTC ETPs at your broker because they aren’t UCITS compliant (that’s true)?

My UK broker (a subsidiary of a G-SIB) would not let me buy US ETFs when I tried, in around September last year.

The EU broker that I use has messaged me recently that ETF trades can no longer be opened on their platform.

The UK broker did say that they can buy them for a managed account, but this doesn’t apply to execution only accounts. One of the funds that they would not buy for me (citing “regulatory restrictions”) is an iShares ETF from Blackrock.

Got it - yes, US listed product is a pariah in much of the rest of the world (I could go on about the reasons, good and bad) Can you buy ordinaries in Germany, Switzerland or Jersey? There are Bitcoin funds (non-UCITS) from those three jurisdictions available … no idea on the retail side though.

In the UK we face the additional issue of the FCA having banned the sale of "cryptocurrency-related “derivatives” (incl ETFs) to retail investors. Which puts investment managers like me in the awkward position of having to avoid the topic entirely with all my clients. Including the ones that already hold Bitcoin directly themselves, via one of the many self-custody options.

So the problem is layered. There is the US ETF restriction, but in addition the ban on “cryptocurrency-related derivatives”. The whole thing is a giant paradox, as it is creating a parallel system, where people with a early interest in Bitcoin are being forced to proceed without any advice or custody options, out with self-custody. Personally, I believe that self-custody of the actual Bitcoin is the best way to go, but the FCA seems to have created a situation doing the opposite of their intention…

It is a strange world.

Germany and Switzerland, yes.

The Bailiwick of Jersey does not have a market that I can see, although it is a UK sovereign dependency.

The “no more expanding trades” message includes structured products.

The closest I came to holding a bitcoin ETF was putting one on my watchlist.

If it was easy to hold, I would have a small holding of some description.

Helpful thanks – Didn’t know how the FCA restrictions landed on retail in terms of other jurisdictions. Interesting!

I get why people are excited about the Bitcoin ETF, although as someone who’s been in the space since 2014 I am not. I had hoped that crypto regulation would have caught up by now in some way that would have made interacting with DeFi more legally plausible (and building DeFi platforms, which is a nightmare from my experience). Seeing “donations” go to a public address held by a regulated ETF is pretty funny though as this same thing could happen in DeFi and in essence those funds could be stranded as well.

Great analysis - learned a lot. Thank you!

Would the ordinals hypothetically come back out someday on a redemption? Like a message in a bottle?!

Was searching a bit for my own answer and found this funny nugget as an aside.